")

High winds, hurricanes, tornados and storms can do a number on your roof. The damage that storms leave in their wake can be catastrophic. Wind damage to a roof is a common problem, in some states it is more frequent than in others. Depending on the state that you live in, your standard home insurance policy should cover roof damage that is caused by wind because the roof is part of the structure of your home.[1]

However, not all wind damage is classified the same by insurers. The source of the wind can determine what your policy will cover and how much you pay out of pocket. The insurance industry can be hard to navigate by yourself. Even if you look closely at your policy to determine beforehand if you need to apply for additional wind damage coverage, a lot can get lost in translation.

CORE Public Adjusters is here to help you. If you find that you need additional assistance to understand your insurance policy and the federal and state laws concerning the kind of wind damage coverage you are eligible for, engaging a public adjuster is the best course of action. A public adjuster is an expert that works on your behalf and deals directly with insurance companies. Their role is to simplify the process for you and advocate the best outcome from your policy.

Now that you know there is help available for you, let’s look at how wind damage to a roof happens, how you can identify it, and how you can find out if your insurance policy covers the damage.

How wind damage to a roof happens

Any wind with speeds over 45 mph can cause some damage to your roof, although winds on this lower end of the spectrum are most likely just to break a few branches and shift some shingles. Anything higher than 50 mph will definitely cause severe roof damage and the prognosis gets worse the higher the wind speed. [2]

Wind flows in different ways, speeds and direction. Winds that are classified as straight-line winds are the most likely to cause roof damage because they occur with thunderstorms. Under-reported straight-line winds are responsible for at least half of all cases of roof damage in the country.[3] These winds can reach speeds of 80 mph and can last for more than half an hour. These winds hit your roof in various patterns, going underneath the shingles and, if powerful enough, ripping them off completely. Sometimes the winds only manage to shift and slightly lift the shingles without ripping them apart. While this might seem like the better devil, this subtle change loosens the shingles, resulting in a leaking roof. And, unfortunately, leaking can go undetected for a long time, wreaking havoc on your home.

Another way that wind damages your roof is by uprooting trees and blowing debris and branches onto your roof. This will definitely cause severe damage to your roof significantly more than the wind itself.

How you can identify roof wind damage

Spotting wind damage to your roof can be difficult if the damage is not an obvious gaping hole in the middle of your house. If you suspect that straight-line winds have damaged your roof after a thunderstorm, the following telltale signs can help you get ahead of the situation.[4]

Leaking roof

If you start to notice some discoloration to your ceiling after a thunderstorm, chances are you have some wind damage and your roof is leaking. To avoid further damage, you will need to get in touch with your insurance company as soon as possible. CORE Public Adjusters can help.

Broken, curled, lifted or missing shingles

If you notice some broken, missing, lifted or curled-up shingles on your roof, you may have had wind damage. This means that your roof no longer has that protective layer, and you are likely to get leaks in these spots.

Some windstorms are strong enough to completely lift the shingles off of your roof. Some areas on your roof are prone to curling shingles because they are high stress points. These areas include the edges, corners, chimney, and the ridge zones on your roof.

If you are lucky enough to spot them, misaligned roof shingles can be the first sign that something is not quite right.

Shingle debris in the gutter

Another subtle telltale sign is loose shingle pieces in your gutter. This will tell you that there is a problem somewhere that is not in your line of vision.

For safety reasons always make sure that you do not climb onto a roof that you suspect has wind or any sort of damage.

How you know if your insurance policy covers the damage

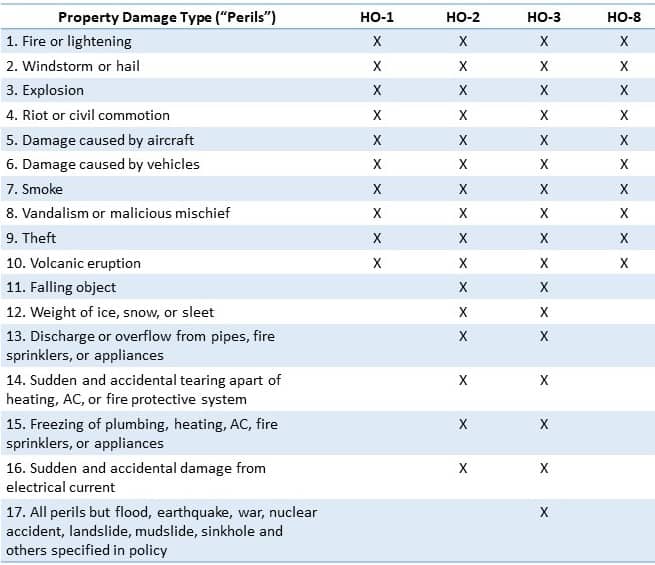

The first step to knowing if your insurance policy covers wind damage to your roof is to understand the four major classifications of property insurance.

According to the Insurance Information Institute, [5] the four types of property insurance you are likely to come across are:

- Limited coverage, or HO-1, which covers against 10 types of property damage disasters (“perils”) but is considered basic insurance and not necessarily a good option for homeowners. In fact, it has been discontinued in most states.

- Standard, or HO-2, provides basic protection against 16 types of property damage disasters.

- Special coverage, or HO-3, is the most popular policy and protects your home for 16 types of disasters and most all disasters except those that are specifically excluded.

- Older Home, or HO-8, protects older homes to include 10 types of property damage disasters, like the HO-1.

The table below gives an in-depth look at which policy covers which property damage disaster. Contact us if you have property damage and are unclear if your policy covers it. We are experts at insurance policy interpretation and can assist you.

The second step is finding or contacting your public adjuster who will go through your home insurance policy to determine if you qualify for a claim.

They will also help you assess the damage and give you steps that you should take to mitigate any further damage. This is an important factor when claiming wind damage from your insurer because the insurer will not pay for any further damage that was caused by negligence.

In general, your insurer is obligated to repair or replace your damaged roof when damage occurs from an insured event, whichever is cheaper. The reality, though, is that wind damage insurance claims are not always smooth sailing. Dealing with a damaged roof and trying to handle an insurer that is nit-picking can be hard to navigate. Hiring a public adjuster will go a long way in ensuring that you get the best possible payout.

Do you have wind damage to your roof?

Contact CORE Public Adjusters. We can assist you with your new, underpaid, or denied claim.

Article References

[1] Insurance Information Institute https://www.iii.org/article/what-covered-standard-homeowners-policy

[2] National Weather Service https://www.weather.gov/media/grb/outreach/SpotterQuickGuide_san.pdf

[3] The National Severe Storms Laboratory https://www.nssl.noaa.gov/education/svrwx101/wind/

[4] American Dream Restoration https://americandreamrestoration.com/roof-wind-damage/

[5] Insurance Information Institute https://www.iii.org/article/are-there-different-types-policies